Despite market volatility and persistent economic uncertainty, nearly all higher educational mega endowments1 produced strong results for the fiscal year ending June 30, 2025. Unlike past years, endowment size was not a meaningful factor in results, as smaller funds performed roughly in line with the median mega endowments based on information tracked by NEPC.

Historically, mega endowments have held a persistent performance advantage over their smaller counterparts, benefiting from larger allocations to private markets and better access to capacity-constrained strategies. That trend flipped in 2023 and 2024; smaller endowments outperformed, driven by greater exposure to public markets, particularly large cap technology companies (such as the “Magnificent Seven”).

In FY 2025, market volatility impacted all endowment strategies, and while public markets continued to produce strong returns, the performance differential between large and small endowments narrowed. The S&P 500 briefly hit bear market territory in April, but the decline was short-lived. In the end, more than two-thirds of mega endowments produced double-digit gains.

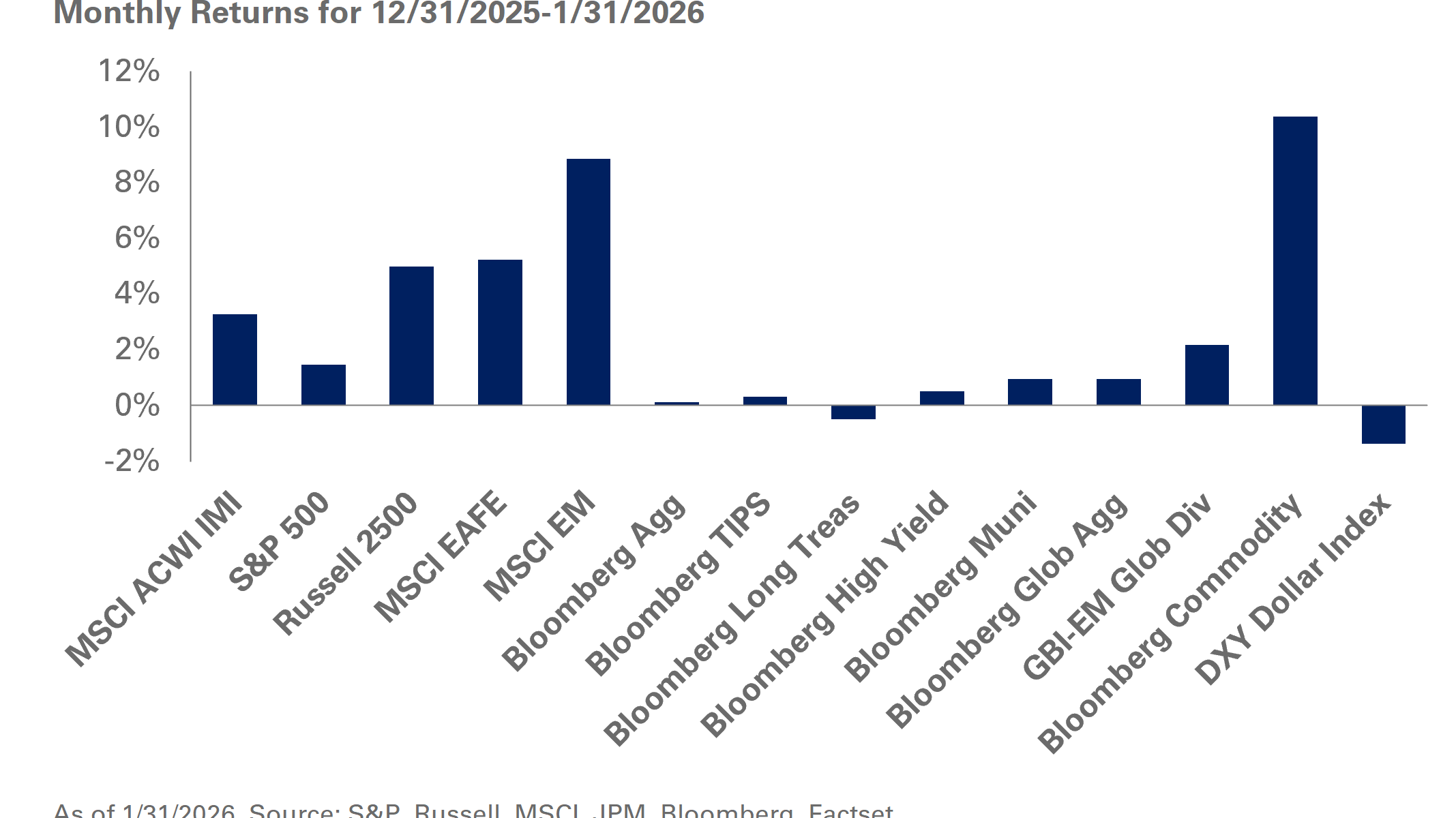

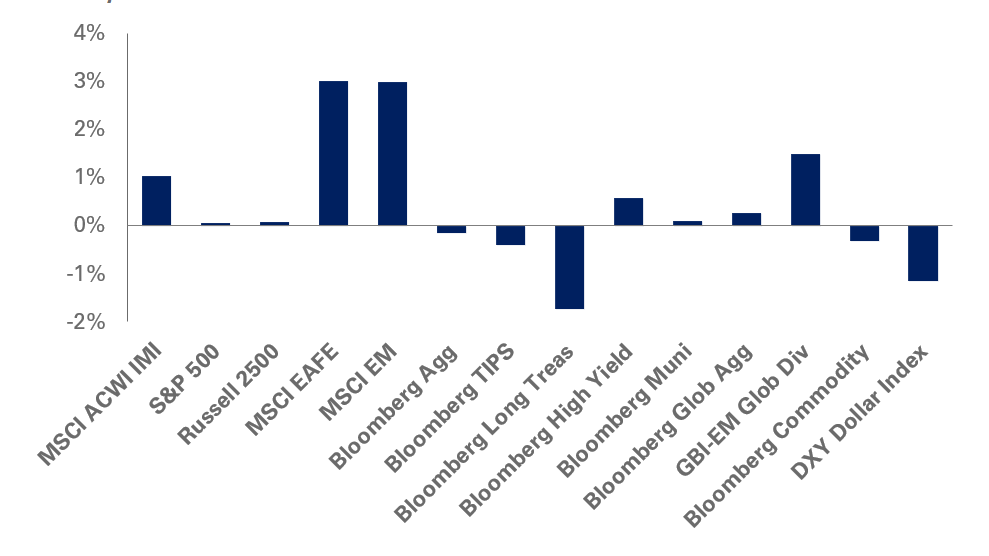

Public equities outperformed alternative assets in 2025 (figure 1), though by a smaller margin than in recent years. Large-cap technology and AI firms were once again leading contributors to results. In addition, non-US equities outperformed US for the first time in several years. Fixed income exposures also added value, with credit sectors producing strong absolute returns. Despite economic uncertainty, fixed income benefited from lower inflation expectations and compression in yield spreads.

1NEPC defines mega endowments as those valued above $1.8B, which represents the threshold for the top 10% of US endowments as listed in the 2024 NACUBO-Commonfund Study of Endowments.

Big, Beautiful Opportunities and Concerns

The most recent year was also notable as higher educational endowments faced new taxation concerns – specifically potential changes to endowment taxation under the “One Big Beautiful Bill Act”2 (OBBBA). Initial versions of the OBBBA proposed new taxation thresholds and significantly higher excise tax rates on endowments, triggering a wave of uncertainty and financial contingency planning.

The most recent year was also notable as higher educational endowments faced new taxation concerns – specifically potential changes to endowment taxation under the “One Big Beautiful Bill Act”2 (OBBBA). Initial versions of the OBBBA proposed new taxation thresholds and significantly higher excise tax rates on endowments, triggering a wave of uncertainty and financial contingency planning.

Fortunately, the final version of OBBBA has had a more limited impact. The tax applies only to a very narrow subset of institutions, and final tax rates were meaningfully lower compared with initial versions of the bill. As a result, for a large portion of the endowment universe, tax exposure has not changed, allowing investment committees to refocus on longer-term portfolio objectives instead of near-term tax mitigation strategies.

Large endowments like Harvard and Yale occupied headlines as they considered secondary sales of their private market portfolios. We believe slowing distributions and shifting market fundamentals have led some institutions to reassess their underlying positions and use the Secondary Market as a portfolio management tool. With large institutions using secondary markets in this manner, we view the stigma of LP led secondaries coming off and think others should view this as a potential tool. However, legal and administrative costs can be significant for secondary transactions and may outweigh the benefits, especially for smaller organizations. As a result, we believe secondary sales are most likely to be relevant for medium to larger endowments or those with specific strategic or tax-driven motivations going forward.

2 H.R. 1, 119th Cong. (2025) (Engrossed in House).

Top Performer Highlights

Among endowments tracked by NEPC, the top performer for FY 2025 was the University of Wisconsin-Madison (managed by the Wisconsin Investment Management Company, or WISIMCO). Wisconsin’s 16.2% annual gain reflects a heavy equity allocation, with 55% in public equity, 31% in private capital, and 12% in real assets. Only 3% of the endowment is allocated to cash/fixed income.

WISIMCO’s investment fund benefited from equity market gains generally and effective stock selection. In the endowment’s recent annual financial report, Michelle Stohler, the WISIMCO CIO, noted that strong stock selection within their public equity allocation in particular, as well as in the private markets, did most to enhance results.

While Wisconsin was the top performer amongst large institutions, the median mega endowment returned 11.3%, in line with the 11.2% gains for the InvestmentMetrics All Endowment Median benchmark. The InvestmentMetrics universe contains data for smaller institutions, indicating relative parity between large and smaller endowments this year.

Looking Forward

In aggregate, small and middle-sized endowments continue to allocate more to public equity markets. According to NACUBO data, endowments in the $100-$250 million range averaged a 51% public equity exposure at the start of FY 2025, significantly higher than the 37% and 24% in public equities held by endowments in the $1-5 billion and >$5 billion ranges, respectively. While we believe this positioning generally helped the smaller endowments, due to strong returns in public equity markets, we did see a broad dispersion amongst investment manager returns. This suggests that active management was a meaningful factor in returns for the top performing funds.

We believe that manager selection will continue to be a driver for the strongest performing endowments going forward. This is particularly true within private markets, where the difference between top and bottom quartile performers is much broader than in public markets. We continue to view private equity and venture capital as long-term drivers of growth, and they should continue to play an important role in portfolios that have long time horizons and limited liquidity needs.

Because companies are waiting longer to go public, we believe the private sector is offering a richer set of opportunities at different points of their growth cycles. The innovation ecosystem that has driven venture capital returns continues to be robust, and there is no shortage of opportunities around AI and related technologies. Rather than avoiding private equity and venture capital, we believe it to be beneficial for investors to approach those sectors with a disciplined, diversified approach, sticking to their strategic targets and annual pacing plans. For those with larger, more developed private market programs, we see Secondaries becoming a potential new tool for consideration.

Once again, we think this year’s trends reinforce the importance of diversification in endowment portfolios. We believe the ideal endowment portfolio targets some form of spending-plus-inflation return, with a level of volatility that matches the institution’s needs. Diversification with a long-term vision can be excellent tools to achieve those goals, even though the performance of various asset classes may ebb and flow over time.